The textile industry has always been global in nature. Raw materials are sourced from one region, processed in another, manufactured elsewhere, and eventually sold across international markets. For decades, this model was built on a relatively simple principle: optimise for efficiency and cost.

Today, that equation is changing.

Over the last few years, a combination of geopolitical tensions, supply chain disruptions, shipping route uncertainties, energy market volatility, and evolving trade agreements has fundamentally altered how businesses think about sourcing and manufacturing. What was once considered a highly efficient global system is now being re-evaluated through the lens of resilience, reliability, and long-term sustainability.

For the polyester yarn industry, these developments are particularly significant.

Unlike many other textile segments, polyester sits at the intersection of manufacturing, logistics, global trade, and energy markets. A disruption in shipping routes, a spike in crude oil prices, or a change in trade policy can have direct implications for raw material availability, production costs, export competitiveness, and ultimately customer demand.

As global buyers increasingly prioritise supply chain security alongside cost competitiveness, the textile industry is entering a new phase—one where manufacturing excellence alone is no longer enough. The ability to navigate a rapidly changing global environment is becoming an equally important competitive advantage.

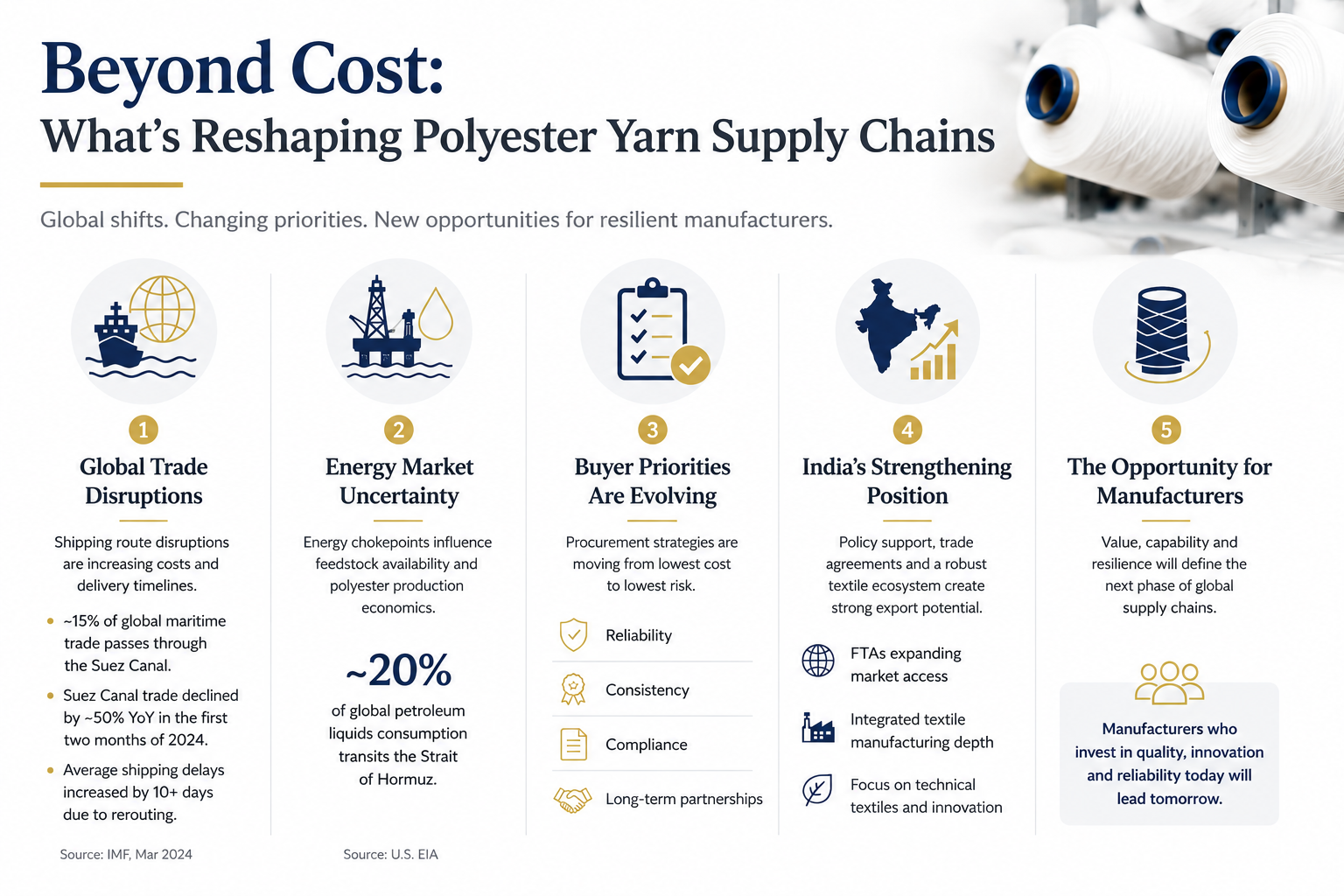

The New Geography of Textile Trade

The global textile industry has experienced a series of shocks over the past five years that have forced businesses to rethink long-standing assumptions. The COVID-19 pandemic exposed the vulnerabilities of highly concentrated supply chains. Factory shutdowns, port congestion, container shortages, and labour disruptions demonstrated how quickly global trade networks could be affected by unforeseen events.

Just as supply chains began stabilising, fresh challenges emerged. Geopolitical tensions, conflicts affecting critical shipping corridors, and changing trade relationships introduced new uncertainties into international commerce.

As a result, textile buyers are increasingly asking different questions than they did a decade ago.

Instead of focusing solely on cost, procurement teams are evaluating:

- Supply chain resilience

- Delivery reliability

- Geographic diversification

- Manufacturing consistency

- Long-term supplier stability

- Trade and tariff advantages

The conversation has shifted from simply identifying the lowest-cost producer to identifying the most dependable manufacturing partner. This change is reshaping sourcing decisions across the global textile industry.

Why Polyester Is More Exposed Than Most Textile Segments

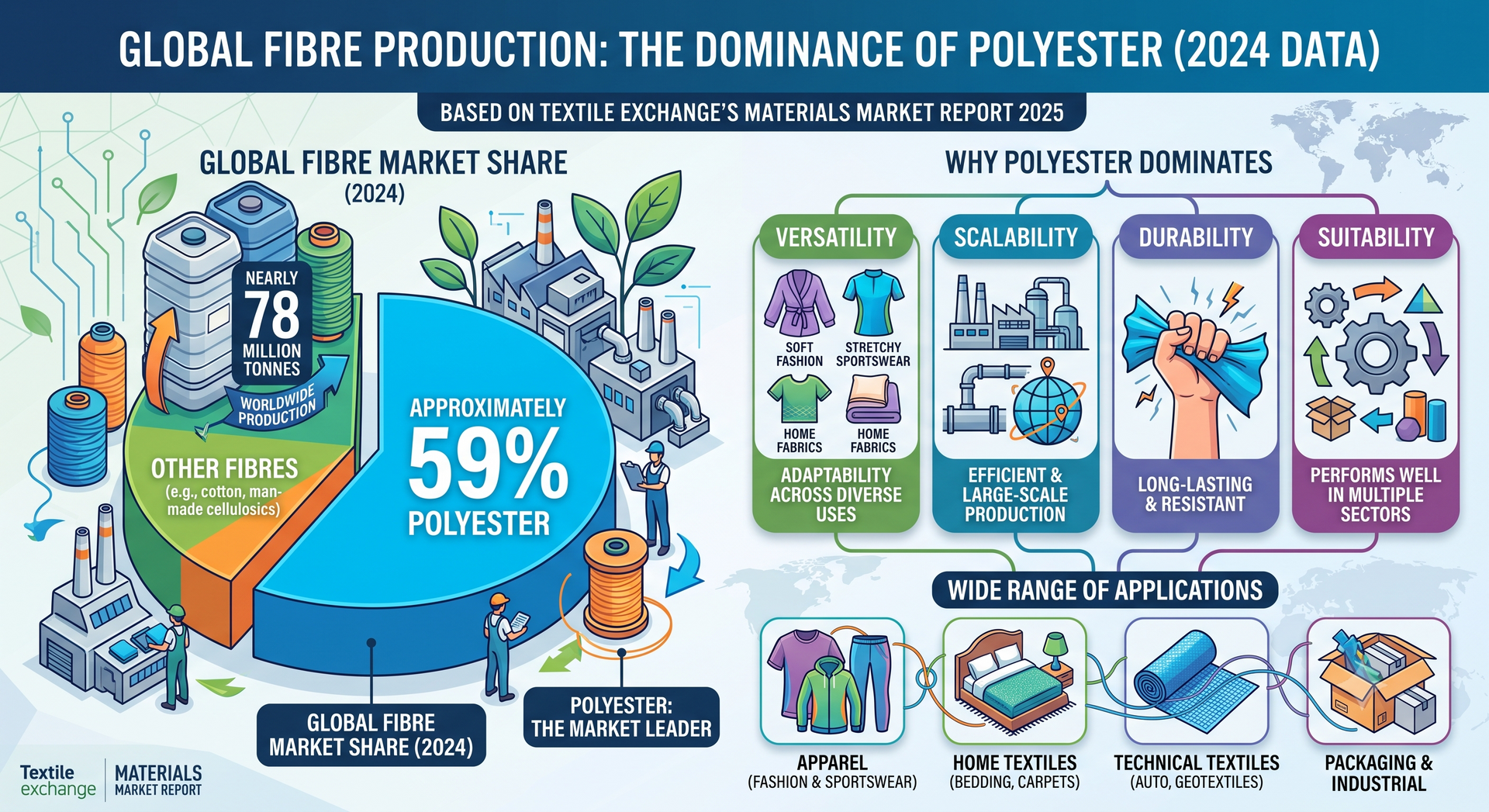

Polyester remains the world's most widely used fibre, making developments in this sector especially important for the broader textile ecosystem.

According to Textile Exchange's Materials Market Report 2025, polyester accounted for approximately 59% of global fibre production in 2024, with worldwide production reaching nearly 78 million tonnes. This dominance reflects polyester's versatility, scalability, durability, and suitability across a wide range of applications.

From apparel and home furnishings to automotive textiles, carpets, geotextiles, industrial fabrics, filtration systems, and technical textiles, polyester has become the backbone of modern textile manufacturing. However, polyester's strengths are also accompanied by unique vulnerabilities.

Unlike cotton, polyester originates from petrochemical feedstocks derived from crude oil. This creates a direct connection between the polyester industry and global energy markets.

Consequently, factors such as:

- Crude oil prices

- Petrochemical production

- Maritime logistics

- Freight costs

- Energy security

can all influence polyester economics.

This makes polyester one of the textile segments most exposed to developments beyond the traditional textile value chain.

Red Sea Disruptions: A Wake-Up Call for Global Supply Chains

Why the Strait of Hormuz Matters to Polyester Yarn Manufacturers

What This Means for Manufacturers Like Jiwarajka

The changing global landscape presents both challenges and opportunities for polyester yarn manufacturers.

As buyers place greater emphasis on reliability, consistency, and long-term partnerships, manufacturers must increasingly compete on more than just production capacity.

For companies such as Jiwarajka, this shift reinforces the importance of value-added polyester yarn solutions designed for diverse end-use applications.

Whether supporting carpet manufacturing, technical textiles, industrial products, or specialised textile applications, the ability to deliver quality consistency and dependable supply is becoming increasingly valuable.

In a world where shipping disruptions, energy volatility, and changing trade dynamics can influence business decisions, manufacturers that combine technical expertise with operational reliability are likely to be better positioned for long-term growth.

The conversation is no longer solely about producing yarn.

It is about helping customers build resilient and efficient supply chains.

From Cost Optimisation to Supply Chain Resilience

Historically, the textile industry operated under a straightforward sourcing model: identify the most cost-efficient supplier and optimise production accordingly.

Today, that model is evolving. Global brands and buyers increasingly recognise that the cheapest sourcing option is not always the most reliable one.

Modern procurement strategies now consider a broader set of factors, including:

- Supply chain stability

- Manufacturing consistency

- Lead-time reliability

- Quality assurance

- Regulatory compliance

- Sustainability readiness

- Geographic risk diversification

In many ways, the textile industry is transitioning from an era of cost optimisation to an era of risk optimisation.

This shift is creating opportunities for manufacturers that can demonstrate operational reliability and long-term consistency.

How FTAs Are Changing Competitive Equations

Trade policy is becoming another important factor shaping textile competitiveness.

These developments demonstrate that future competitiveness will increasingly be influenced not only by manufacturing efficiency but also by market access and trade relationships. For textile exporters, FTAs can create meaningful advantages by improving pricing competitiveness and expanding business opportunities.

Why India Is Emerging as a Strategic Textile Partner

As global buyers reassess sourcing strategies, India is increasingly positioned as an important manufacturing destination.

The country possesses several structural strengths:

- A large and diversified textile ecosystem

- Strong manufacturing capabilities

- Growing synthetic fibre capacity

- Expanding technical textile sector

- Skilled workforce

- Increasing integration with global trade networks

India is also actively investing in the future of textile manufacturing. Government initiatives such as the PM MITRA scheme and the National Technical Textiles Mission are aimed at strengthening infrastructure, encouraging investment, and supporting innovation across the textile value chain.

As demand for man-made fibres and technical textiles continues to grow globally, these investments could help further strengthen India's position in international markets. However, the opportunity extends beyond capacity expansion.

Global buyers increasingly expect manufacturers to deliver:

- Consistent quality

- Reliable supply

- Technical expertise

- Transparency

- Responsiveness

- Long-term partnership capabilities

Manufacturers that can meet these expectations will be best positioned to succeed in the next phase of global textile growth.

Sources

- Textile Exchange – Materials Market Report 2025

- Textile Exchange – Materials Market Report 2024

- International Monetary Fund (IMF) – Red Sea Attacks Disrupt Global Trade

- U.S. Energy Information Administration (EIA) – Strait of Hormuz Energy Transit Data

- Government of India – PM MITRA Scheme

- National Technical Textiles Mission (Government of India)

- India–UK Free Trade Agreement official announcements and summaries

- India–UAE CEPA documentation and trade summaries